Drawing on that database and other relevant sources, this report examines rates of employer ownership by race and ethnicity and reaches the following conclusions:

- Black-owned employer-businesses earn nearly five times more in revenue per worker than Black-owned non-employer-businesses, making it an attractive pathway to wealth for Black Americans. Yet, while ownership rates are similar across racial and ethnic groups for non-employer-businesses, white Americans are seven times more likely than Black Americans to own employer firms.

- Lack of work experience with a business owned by a family member seems to partly explain why few Americans work for Black-owned businesses. Census data shows that most business owners were born in the 1950s and 1960s, so their parents would have been born in the 1930s and 1940s and therefore at a time when Black Americans faced extreme discrimination in a variety of markets and faced limited entrepreneurial opportunities. Thus, not surprisingly, Black Americans are the least likely to say their family owned a business while they were a child; however, employer-firm ownership rates nearly triple among Black Americans who did grow up with a family-owned business compared to those who did not. Other evidence shows that prior work experience with a family-owned business is particularly important in predicting current ownership, suggesting that the accumulation of business-specific knowledge is more valuable than either the transmission of the business itself or accumulated parental wealth.

- Limited access to external credit seems to be a major reason why there are not more Black-owned employer businesses. The Gallup survey finds that Black Americans are the most likely to report difficulty and lack of success when applying for business financing. Other evidence suggests this difficulty is partly but not entirely the result of underlying credit history. Additional evidence finds that Black entrepreneurs face inexplicably high rates of rejection for business loans and are disproportionately deterred from seeking financing because of rejection fears. Consistent with this evidence, the Gallup data shows that Black business owners are 4.5 times more likely than white business owners to say they were treated unfairly while trying to obtain a loan or financing.

- Black Americans score above the U.S. mean on entrepreneurial traits. These traits, such as confidence and determination, are associated with business ownership and success. Other characteristics that might be thought to predict business ownership and success, such as literacy and numeracy, are, in fact, not predictive and therefore cannot explain gaps in business ownership by race.

Thus, Black Americans face distinct barriers in accessing capital and work experience alongside small business owners, and these factors contribute to low employer-firm ownership rates. Investors, lenders, and policymakers should seek ways to get more capital into the hands of Black entrepreneurs and ways to help Black youth get more training opportunities alongside small business owners. One potential way to increase Black entrepreneurs’ access to capital is to eliminate discriminatory lending practices, but further research is needed to establish the prevalence and importance of this channel, and it would require the cooperation of large lending institutions.

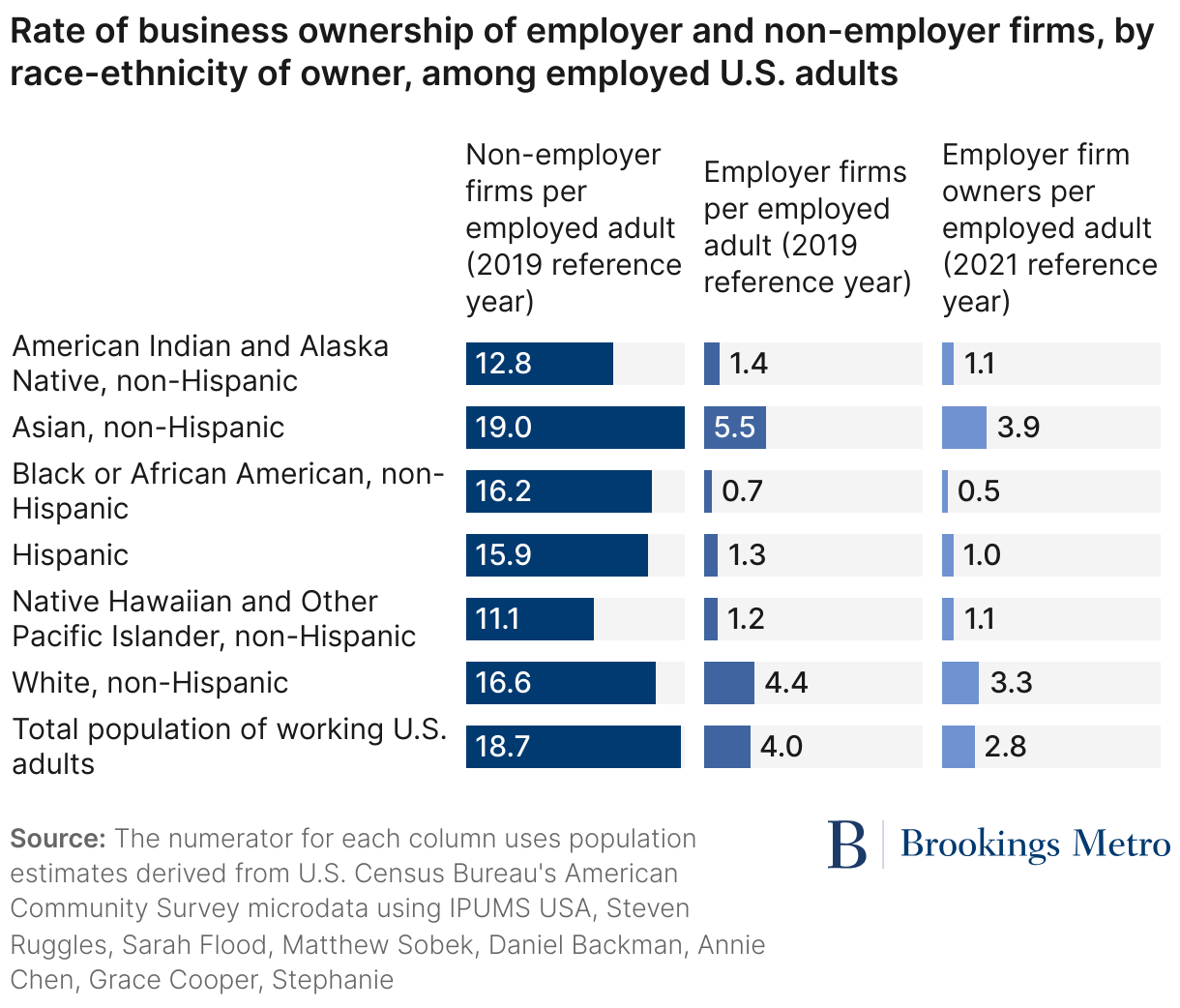

Employing others is much less common than owning a business, especially among American Indian, Black, and Hispanic Americans

[The Census Bureau produces demographic data for employer businesses, based on a large sample of firms that pay employer taxes, and a separate database for non-employer-businesses, which matches administrative records with census data to identify race. Employer firms are much less common. In 2020, the latest records available for non-employer-businesses, there were approximately 19 non-employer-businesses per 100 working U.S. adults but only four employer firms. In 2021, there were only 2.8 owners of employer firms per 100 adults.]

Employing others is a key source of wealth creation for all racial and ethnic groups, but it is much less common among American Indian, Black, and Hispanic Americans.

Entrepreneurship — defined as business ownership — is relatively common across groups, and rates of ownership are similar between racial and ethnic groups for non-employer-businesses.5 There are roughly 16 non-employer-businesses with majority ownership by a Black American for every 100 Black workers. This ratio is similar for Hispanic and white Americans and only slightly higher (19) for Asian Americans. The lowest rates are found among non-Hispanic American Indian and Pacific Islander populations, but even these rates are, at their lowest, two-thirds of the rate for white Americans.

Yet, when it comes to employer firms, ownership is rare, and there are very large discrepancies in ownership rates across racial and ethnic groups. The most accurate data report statistics by the characteristics of the owners (not the firms), and these are available from the 2022 Annual Business Survey, which refers to businesses operating in 2021. That year, just 0.5% of Black American working adults owned a business with employees, compared to 1% of Hispanic Americans, 1.1% of American Indian and Alaskan Natives, 3.3% of white Americans, and 3.9% of Asian Americans. The Black employer firm rate is just one seventh the white rate and one eighth the Asian rate.

Rate of business ownership of employer and non-employer firms, by race-ethnicity of owner, among employed U.S. adults

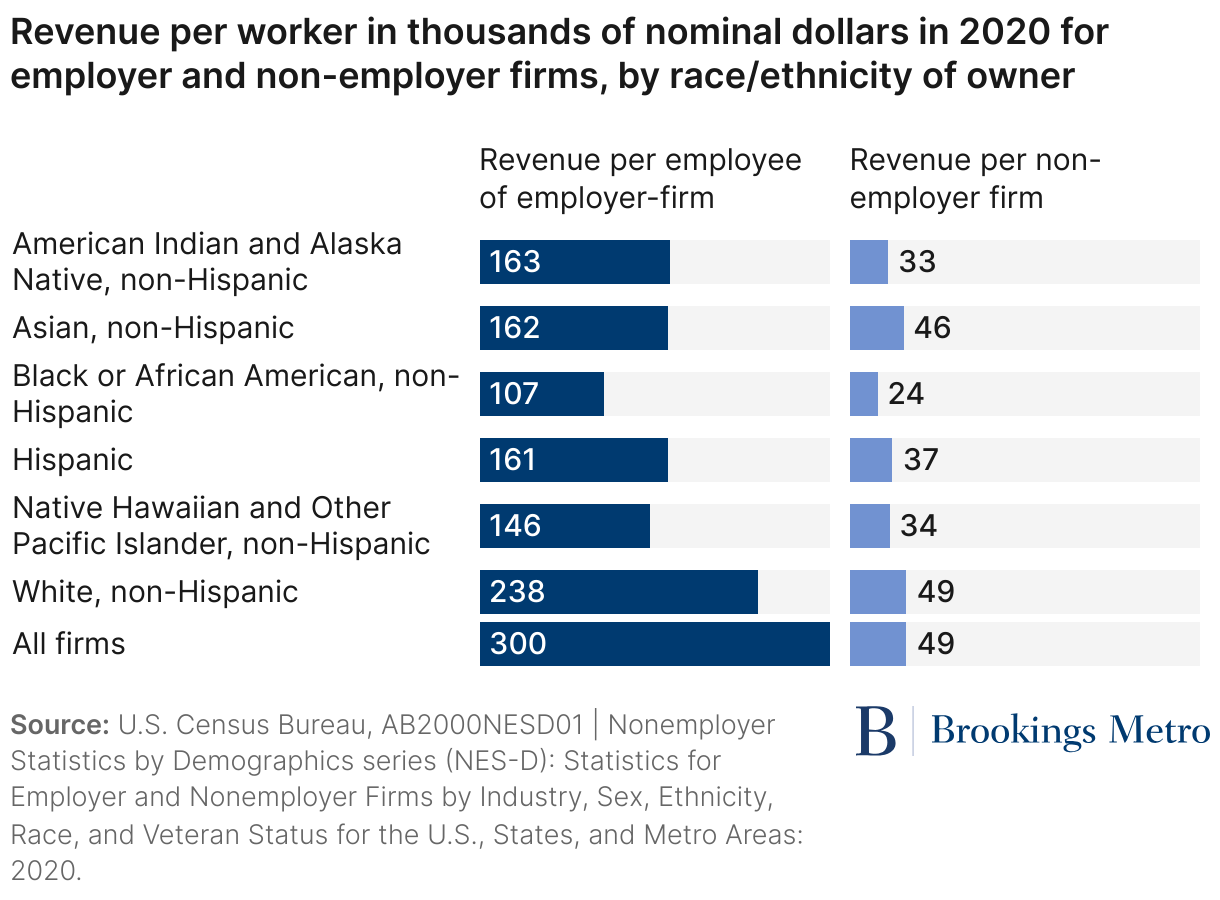

Employer-firm ownership contributes to rising wealth because revenue per firm and revenue per employee is much higher for employer firms relative to non-employer-businesses overall and for each racial group. Revenue per firm is approximately 40 times higher for Black-owned employer firms ($1 million) compared to Black-owned non-employer-businesses ($24,000). This difference is partly due to the number of employees, but a large gap persists even after accounting for the number of workers. On a per-employee basis, revenue is 4.5 times higher for Black-owned employer firms ($107,000) compared to non-employer-businesses. Thus, unless the profit margins of non-employer-businesses are dramatically higher, which is unlikely, employer firms generate greater income and wealth.6

Revenue per worker in thousands of nominal dollars in 2020 for employer and non-employer firms, by race/ethnicity of owner

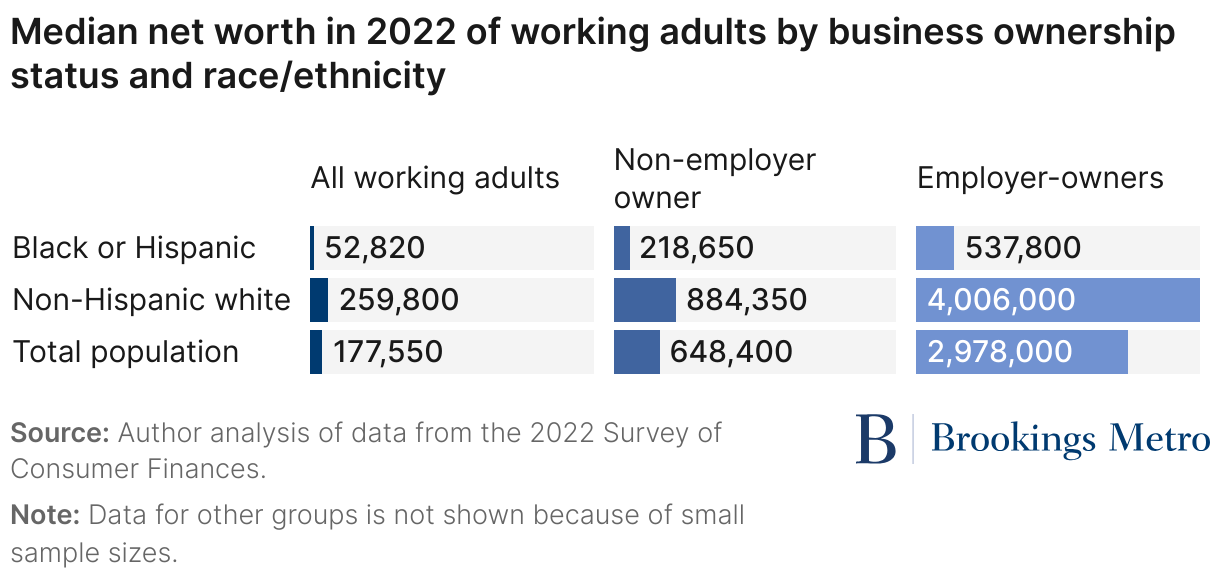

Evidence from the U.S. government’s most detailed survey on wealth (the 2022 Survey of Consumer Finances) confirms that net worth is much higher among working U.S. adults who own an employer firm relative to non-employer owners and all adults, and this appears to be true across racial and ethnic groups, though the sample sizes are too small to report Black and Hispanic Americans separately. Median net worth is approximately 10 times higher for Black and Hispanic Americans who own an employer business relative to all employed Black adults and approximately twice as high relative to those who own a non-employer business.

Median net worth in 2022 of working adults by business ownership status and race/ethnicity

We evaluate several potential explanations for low employer-firm ownership rates among Black Americans

Given the large advantages associated with employer firms, why are ownership rates so low for Black Americans? We cannot definitively answer this question, but we consider and evaluate three possible explanations:

- The intergenerational transmission of wealth and entrepreneurship

- Barriers to accessing loans or investment capital through financial markets

- Gaps in personality traits or management practices

The primary data for this article come from the 2023 Gallup Pathways to Wealth Survey, which is described in a detailed companion report.7 Between Sept. 21 and Oct. 30, 2023, Gallup surveyed U.S. adults and oversampled business owners, using sample from the Gallup Panel and the universe of recipients of Paycheck Protection Program fundings. The final sample size of 9,828 working U.S. adults included 3,117 “owners,” defined as anyone who received at least some income in the prior month from a business they own. Among these owners, 976 reported that they employed at least one employee other than themselves. This final pool of respondents was weighted to be representative of working employer-business owners and non-owners of employer businesses among the U.S. employed adult population.

1) The intergenerational transmission of wealth and entrepreneurship

There is a large and persistent gap in median wealth between Black Americans and others. Recent modeling work from economists at the London School of Economics suggests that low rates of Black entrepreneurship explains much of that gap. Nonetheless, while ownership begets wealth, successfully launching an employer firm often requires wealth. Personal savings is the most common source of startup funding among business owners in the Gallup survey, which showed that 73% of entrepreneurs who needed startup capital used their own savings. So, the relatively low net worth of Black Americans almost certainly hampers entrepreneurship. The large gaps in wealth between White and Black Americans has been explored in extensive academic research, showing the gap was even greater in the aftermath of the Civil War.8 During much of the twentieth century, business ownership was hampered in Black communities by informal and formal restrictions on lending, business ownership, and the practice of professions. This legacy has meant that Black Americans are the least likely racial and ethnic group to say that their family owned a business while they were growing up. Family ownership rates are roughly half as large for Black Americans relative to Asian or white Americans, according to the Gallup data.

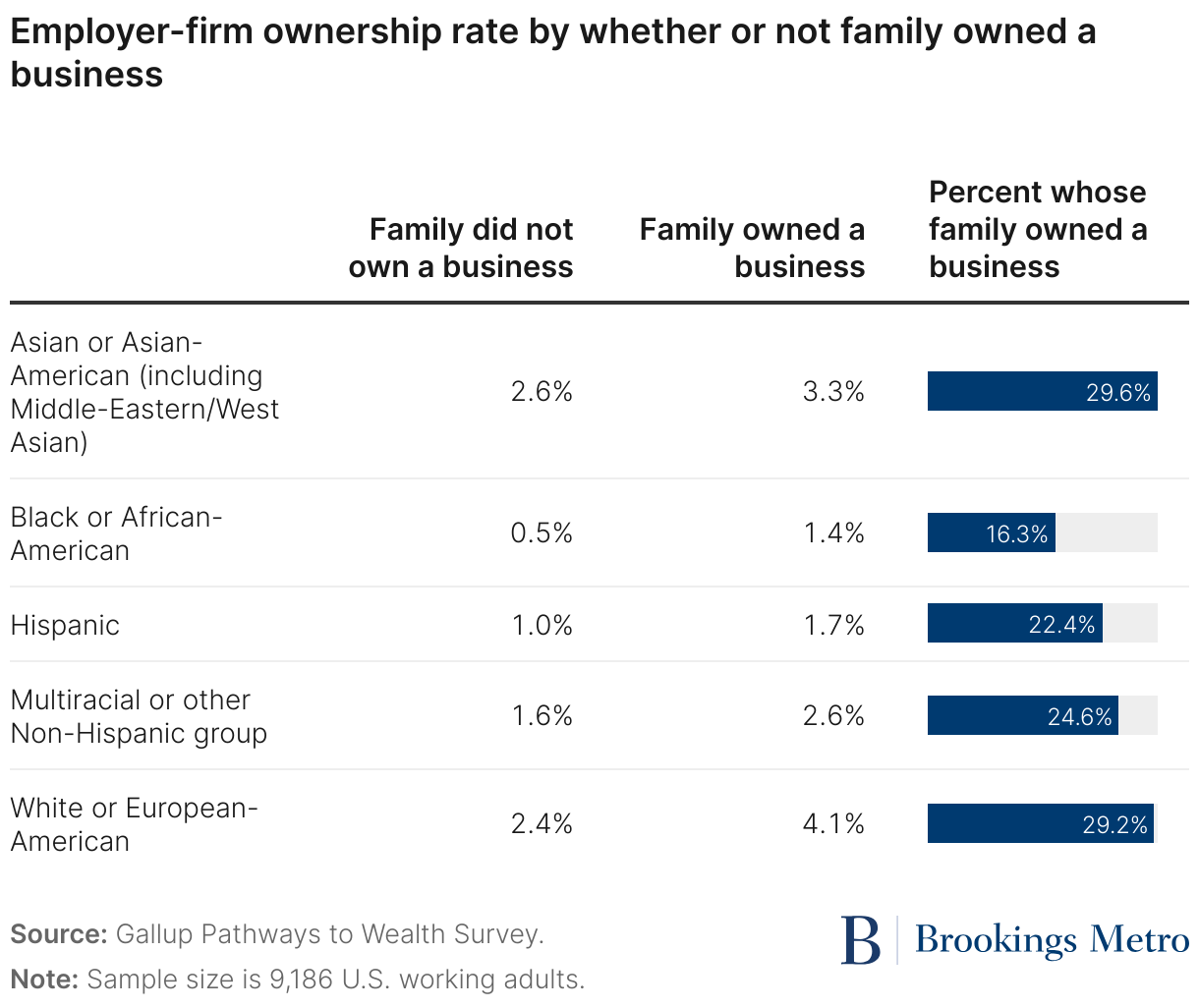

Prior work has found that working for a family-owned business greatly increases the odds that one later owns one’s own business.9 There is evidence of this in the Gallup survey. It does not ask whether the respondent worked for his or her family’s business — though prior work suggests that many people have.10 In any case, across every racial and ethnic group the employer-firm owner rate is higher for those whose family owned a business.11 Notably, the rate is 2.7 times higher for Black Americans, the highest gap among all groups.

Employer-firm ownership rate by whether or not family owned a business

There are several channels by which parental or family business ownership in childhood may raise the odds of someone becoming a business owner: inheritance, wealth, and entrepreneurial knowledge.

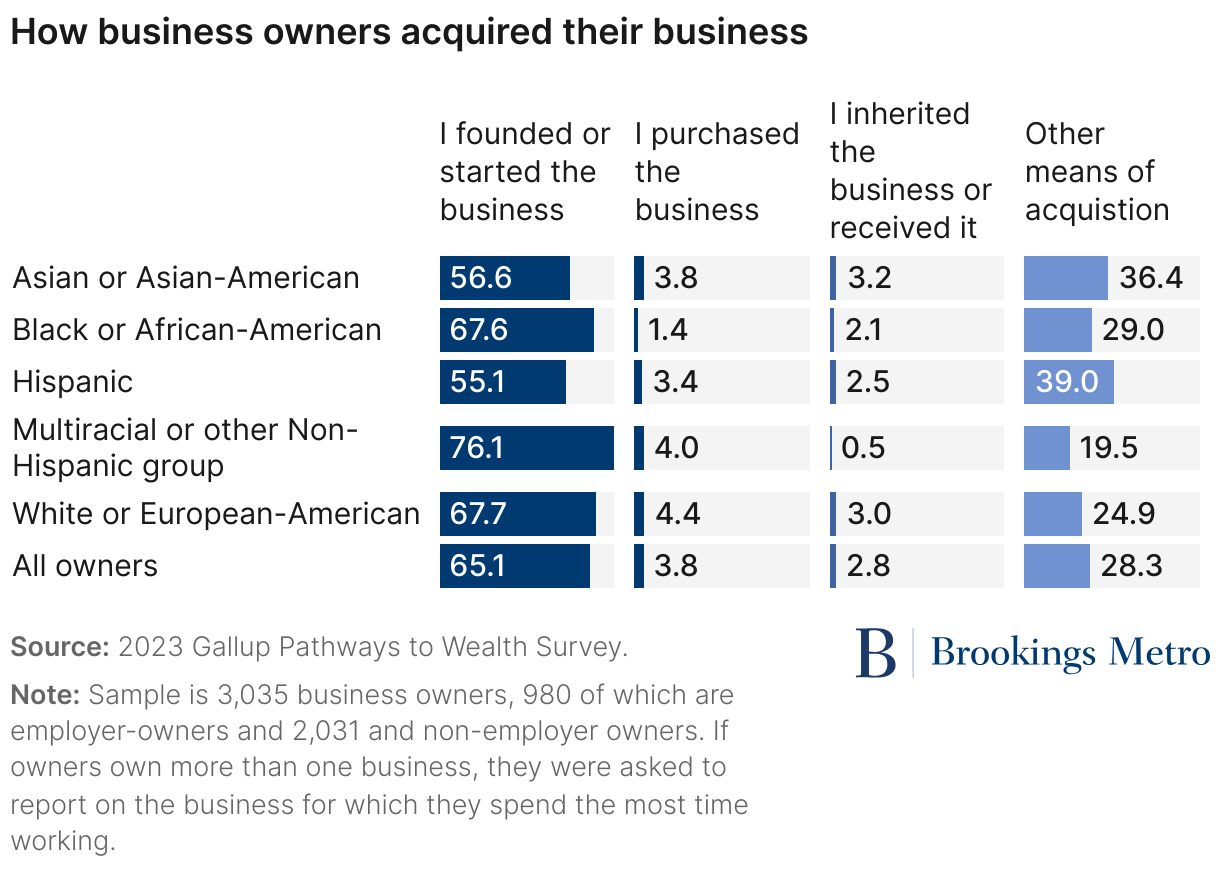

One channel is that the family business can be directly passed on or inherited. This is a somewhat rare occurrence. In the Gallup data, only 2.8% of business owners inherited or received their business from family. A majority of owners started their own businesses, including nearly three-quarters of employer-owners. Indeed, owners whose families owned businesses were more likely to start their own firms than owners whose families did not own businesses (70% vs 63%), suggesting that something other than the direct transmission of the business is important.

How business owners acquired their business

While parental wealth could play an important role in giving owners start-up funding, there is evidence that it usually does not. A U.S. Bureau of Labor Statistics (BLS) National Longitudinal Survey initially started in 1997, known as the NLSY97 survey, is a follow-up project to the BLS’ NLSY79 survey. The NLSY97 surveyed a representative sample of Americans born between 1980 and 1984. In 2021, it asked respondents born between 1980 and 1984 whether they were self-employed, and, if so, whether they employed other workers. Five percent gave responses indicating that they were both self-employed and employed other workers. The parental wealth associated with these respondents — measured back in 1997 — predicted higher educational attainment, but it did not predict significantly higher employer-firm ownership rates.

Similar evidence comes from the Gallup survey. It asked the extent to which the family faced financial difficulty: “When you were growing up, which statement best describes your family’s economic status?” Answers were placed on a four-point scale with the following options:

- It was often difficult for my family to live on their income

- It was sometimes difficult for my family to live on their income

- My family was able to get by on their income

- My family was able to live comfortably on their income

Controlling for age, race, ethnicity, sex, and education, there is no significant difference between the most comfortable arrangement and any of the others in predicting employer-business ownership.

Instead, the most likely channel through which parental family ownership during childhood raises current ownership rates of adults is through knowledge and experience. Respondents whose families owned businesses report significantly higher confidence in their own ability to start or operate a business, using either of the two entrepreneurial self-efficacy measures described above. Furthermore, the NLSY79 survey asked respondents if they had ever worked for a business owned by their family. Those who had were much more likely to report ever owning an employer business. However, for those who did not work for the business, having a family-owned business did not raise the odds of eventually becoming an owner of an employer business. In the NLSY79, 6.8% of Black Americans reported that they worked for a family business, compared to 11.4% of white Americans.

2) Barriers to accessing loans or investment capital through financial markets

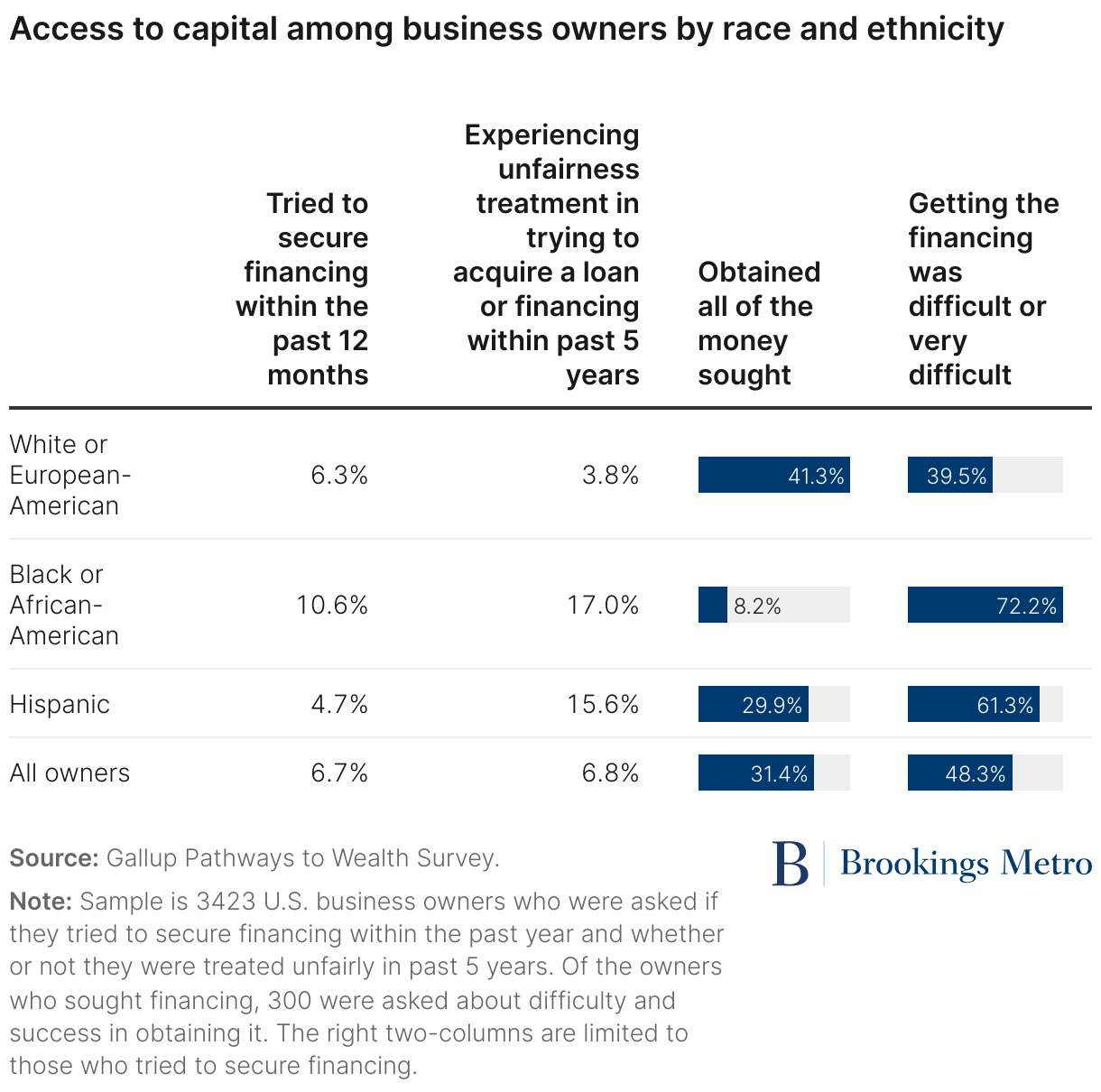

For entrepreneurs requiring external capital, the obvious solutions are to pursue it through investment or loans, but social science evidence suggests that Black owners face challenging and unfair financial markets when it comes to business lending.12 Black owners are 4.5 times more likely to say they were treated unfairly in trying to acquire loans or financing over the past five years than white owners. Hispanic owners reported similarly high levels of unfair treatment. For Black owners who sought financing last year, few (8%) obtained all of the money sought, compared to 41% of white owners, and a very high percentage (72%) reported difficulty obtaining financing, compared to just 40% of white owners.

Access to capital among business owners by race and ethnicity

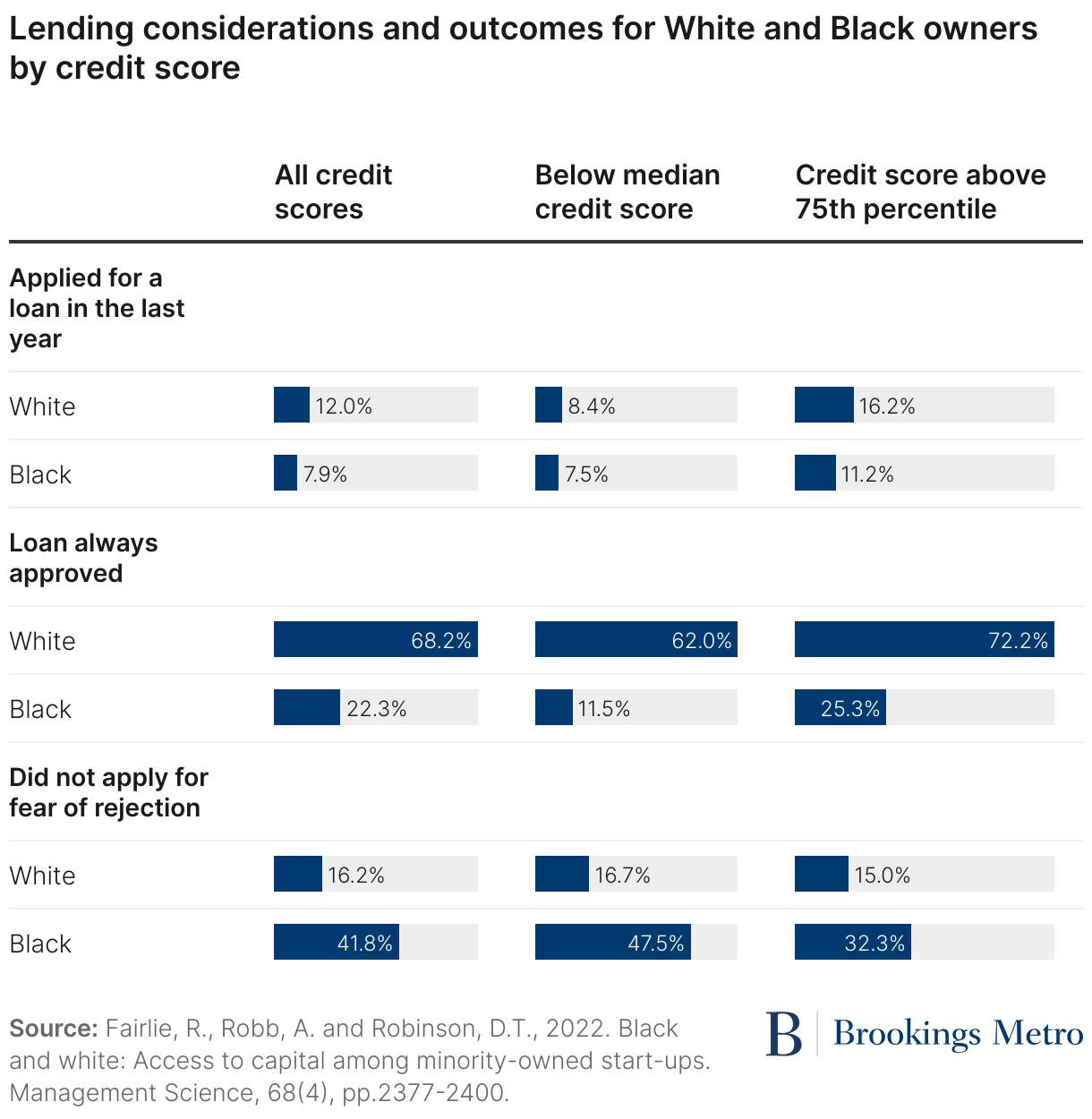

The relative difficulty of borrowing faced by Black business owners has been found in previous work by the economists Robert Fairlie, Alicia Robb, and David Robinson. Their analysis finds that credit score gaps between white and Black Americans are large and explain about one-third of the revenue gap between white-owned and Black-owned firms. At the same time, they find that much of the gap is unexplained by credit history, and even Black owners with high credit scores confront low success rates and high fears of rejection when applying for business loans. Those rejection fears seem grounded, in part, by discriminatory treatment in the assessment of Black business loan applications, according to recent evidence.13

Lending considerations and outcomes for White and Black owners by credit score

3) Personality and other enduring traits

Another reason why rates of employer-firm ownership differ by race and ethnicity is that groups could differ in enduring traits that are conductive to launching or sustaining complex organizations, such as employer-businesses. A recent meta-analysis compared the effects of cognitive traits (such as numeracy and literacy) to the effects of emotional intelligence, such as decisionmaking under stressful circumstances, persistence, and the ability to sustain productive social relationships. The authors found that both traits predicted success as an entrepreneur, but emotional intelligence was much more important.14 Likewise, there is strong evidence from the business and psychology literature that other non-cognitive personality traits strongly predict entrepreneurial entrance and success. A recent review by Kerr, Kerr, and Xu finds that having an internal locus of control, self-efficacy, or scoring high on some of the Big 5 personality traits (like conscientiousness) predicts greater or more successful entrepreneurial activity.15

The importance of personality traits to entrepreneurship has been confirmed in a report published by Gallup using the Pathways to Wealth database.16 Using factor analysis, Gallup combined many survey items into measures of the following constructs:

- Entrepreneurial self-efficacy: defined as confidence in the ability to successfully perform the tasks associated with starting and running a business.

- Internal locus of control: defined as the extent to which a person feels they influence the course of their life and can navigate the world competently and predictably.

- Orientation toward social achievement: defined as the extent to which people value cooperating with others to benefit humanity.

- Value placed on personal autonomy: defined as a desire for autonomous, creative work that uses natural talents.

- Personality traits, as measured by the Big 5 personality traits: defined as conscientiousness, agreeableness, openness to experience, emotional stability, and extroversion; Gallup added determination, decisiveness, and boldness to this list since they are related to entrepreneurial activities.

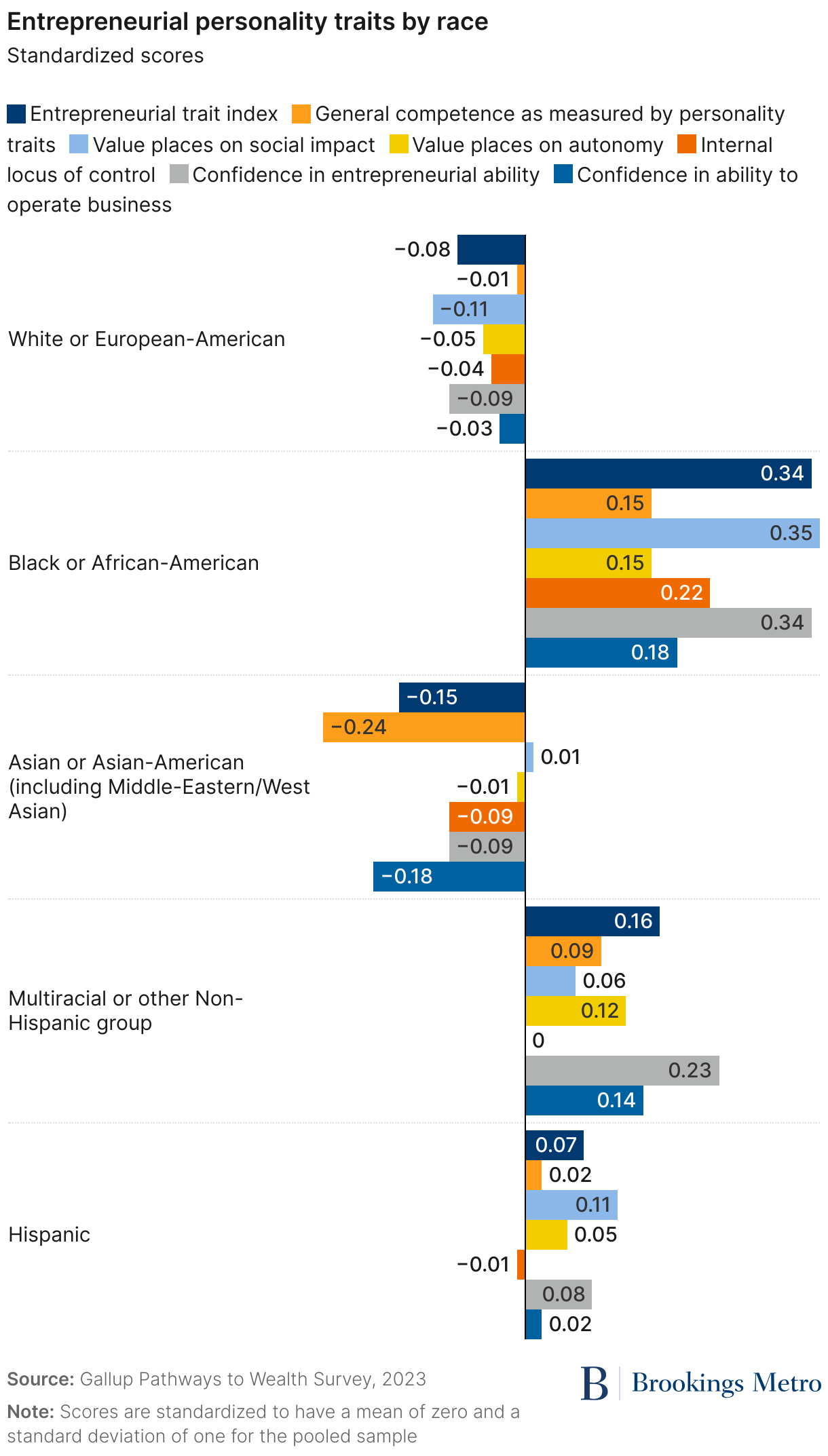

After standardizing each measure, a combined score was calculated based on the mean score for each construct listed above. The final score is highly predictive of interest in becoming an entrepreneur, actions taken to become one, and performance as an entrepreneur. Contrary to the patterns observed in ownership rates, entrepreneurial traits tend to be higher among Black, Hispanic and multiracial workers. Black adults score particularly high on values placed on social impact, having an internal locus of control, and confidence in their entrepreneurial ability (or self-efficacy). Across racial and ethnic groups, the combination of these traits is predictive of higher income, subjective wellbeing, and wealth.

Entrepreneurial personality traits by race

Standardized scores

Another relevant set of traits are those related to cognitive ability, which is measured through performance on standardized tests of numeracy and literacy. Cognitive skills, measured in this way, are closely related to educational attainment, but vary within people with the same levels of attainment, as high school scores on state exams or college entrance exams show.17 In the U.S. adult population, tests of this kind generally show differences across racial and ethnic groups, which have varied over time in ways that are consistent with differences in social resources and political power.18,19 Higher scores on these exams predicts higher income, health, and job performance.20 Yet, the best available evidence — from two data sources — shows that the cognitive ability of owners of employer-firms does not differ from that of non-owners.

The U.S. Bureau of Labor Statistics National Longitudinal Survey of Youth (NLSY-79) followed a representative sample of 7,000 Americans born between 1957 and 1964 through detailed surveys conducted from 1979 through 2020. Starting in 2010, the survey asked if they had ever owned a business and whether that business employed anyone. Cognitive ability, as measured in 1979 using a test developed by the U.S. military, is not significantly related to the probability of ownership after adjusting for sex, age, race, ethnicity, and educational attainment. Another high-quality database, the Program for the International Assessment of Adult Competencies (PIAAC), yields similar results. The PIAAC was administered in the United States in 2012, 2014, and 2017 to approximately 11,226 working-age (16 to 74) U.S. residents. Among those currently employed, their combined scores on math, literacy, and problem-solving are highly predictive of income but not at all predictive of whether or not they owned a business with employees. The unconditional mean employer-firm ownership rate is not significantly different as cognitive performance increases. Also, there is no significant difference after adjusting for the demographics listed above.

Thus, neither cognitive ability nor personality traits can explain why employer-firm ownership rates are low among Black adults. If anything, they should be higher.

Conclusion: Personal net worth, childhood exposure to business, credit history, and lending practices are behind low ownership rates

Low personal net worth and poor or thin credit history, unfair treatment by lenders or investors, and more limited opportunities for working in a family-owned business are among the reasons why Black Americans are less likely to own businesses, and, therefore, why more Americans do not work for Black-owned firms. There may be other reasons, but differences in personality traits and cognitive skills — meaning literacy and numeracy — are not among them. In fact, Black Americans demonstrate a significantly higher proclivity than other groups for entrepreneurship based on self-reported personality traits that are predictive of business owners and success.

Several insights that stem from these conclusions could spur more equitable entrepreneurial opportunities. First, private and public sector leaders should seek ways to test for bias in capital markets and correct for it. Doing so could spur greater confidence for Black entrepreneurs that their efforts to get capital will be handled fairly. Second, secondary schools and companies should make efforts to replace lost learning opportunities when it comes to running a business. For the many Black children and young adults whose families do not own businesses, high school courses, jobs, and internships at small businesses could provide valuable experience, especially if youth are given the opportunity to work closely with owners. Finally, efforts to bolster the perceived value of Black communities, and the wealth of the Black population generally, could foster greater real estate and small business wealth, leading to a virtuous cycle that spurs future entrepreneurship.

We realize this work leaves many questions about entrepreneurship unanswered, and we intend to address some of them in future work. Longitudinal research could clarify what percentage of self-employed workers or non-employer owners eventually hire workers to help with their current business or a new one. We would also like to know what characteristics of entrepreneurs and businesses predict the development of non-employers into employers.

There are other questions more closely related to policy. For instance, we would like to study how specific lending practices deter Black entrepreneurs and measure the prevalence of discrimination, defined as racial bias in lending decisions. We would also like to explore the role of local government in supporting businesses. Data from the Pathways to Wealth Survey suggests that very few employer-owners receive subsidized loans or grants from either state or local governments.21 Whether and when such things should be left to markets is subject to debate. Other actions by local governments, chambers of commerce, and non-profits may be less expensive but still helpful, such as arranging for networking events, marketing campaigns — for a destination cluster of businesses, for example — or forums for learning opportunities. Local governments and leaders may play a role in setting up or removing barriers to the creation of business incubators that offer entrepreneurs these and other resources.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}